While cash is king when running or starting a business, credit cards are queen when it comes to fast, convenient ways to accept payments from your customers. After all, 82% of American adults had a credit card in 2023, according to the Federal Reserve.

If your business isn’t set up to accept credit card payments, you could be missing out on potential sales. Whether you’re running a service business, a brick-and-mortar store, or you have an online shop that needs to accept digital payments, we’ll help you understand how credit cards are processed, what equipment you need to process them, and what payment software does for your company. If you’re looking for a way to get paid quickly and manage your business finances, QuickBooks Money makes it easy.

Queue up your card readers!

How credit card processing works

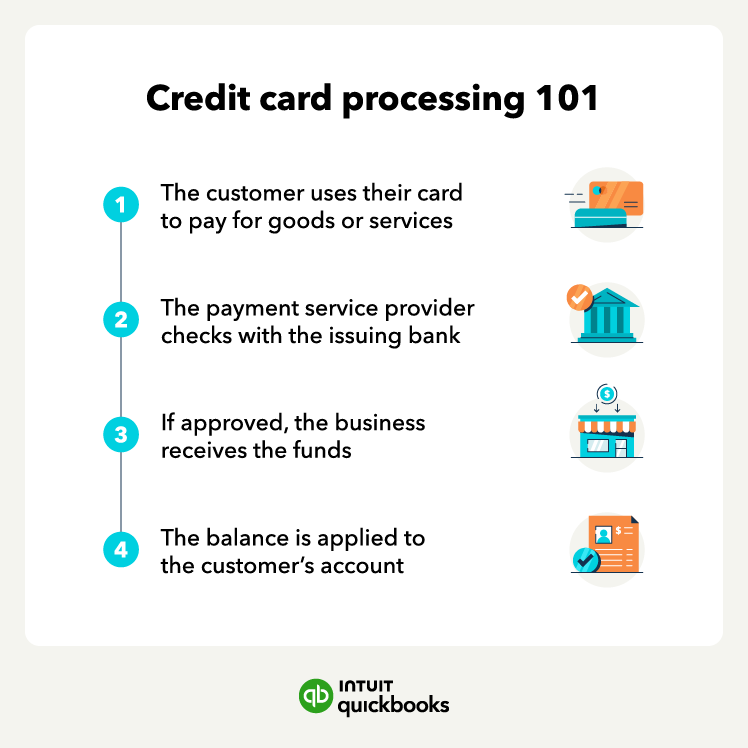

The process seems pretty simple on the surface: a customer swipes their card and then you get your money. But there’s actually quite a bit of complexity involved in credit card transactions.

Let’s break it down into three main parts: authorization, authentication, settlement, and clearing.

1. Authorization

When a customer pays with a credit card (by inserting, swiping, or tapping on a terminal or using it online on a website or through a digital wallet like PayPal), the merchant’s payment processor reaches out to the issuing bank through a credit card network. Then, the credit card network sends an authorization request to the bank that issued the card.

Those authorization requests include:

- The credit card number

- The card’s expiration date

- The CVV (Card Verification Value) security code (the 3-digit code on the back of the card

- The payment amount

- Optional: The billing address (as a part of the fraud-prevention Address Verification System (AVS))

Next comes the authentication process.

2. Authentication

Once the authorization request arrives at the issuing bank, they verify that the card number, billing address, and CVV match. Then the bank approves or declines the request. Denials can be based on a lack of funds, if a card is expired, if the card has been reported stolen, or if there is fraud suspected.

That response is bounced back through the same channels and reaches the merchant.

If the transaction is approved, the customer will see a hold on the purchase amount on their account, and at this stage, the transaction will be pending. At the end of the day, the merchant will start the settlement and clearing process to complete the transaction.

3. Settlement and clearing

At this point in the transaction, the customer’s part in the process is over. Batches of authorizations are sent to the processor at the end of the day or another preset time, though there are some processors that offer real-time processing that don’t need to be batched. This may require manual processing or it may happen automatically depending on which processor you use. The processor will then request each issuing bank to transfer the funds to the merchant account.

This process usually takes a day or two. Once payments are processed, the merchant will receive their funds. The payment received will be what the seller has charged their customer for the goods or services they provided, minus any fees associated with processing the payment.

3 common ways to take credit card payments (and what you need for each)

Now that we’ve covered how processing a credit card payment works, let’s look at how to take credit card payments using one or more of the following methods.

No matter how and where you take credit card payments, you’ll need a few things including:

- A merchant account

- A payment service provider (PSP)

- Card reader hardware and/or software

Luckily, it can be pretty easy to get all of these set up and working together.

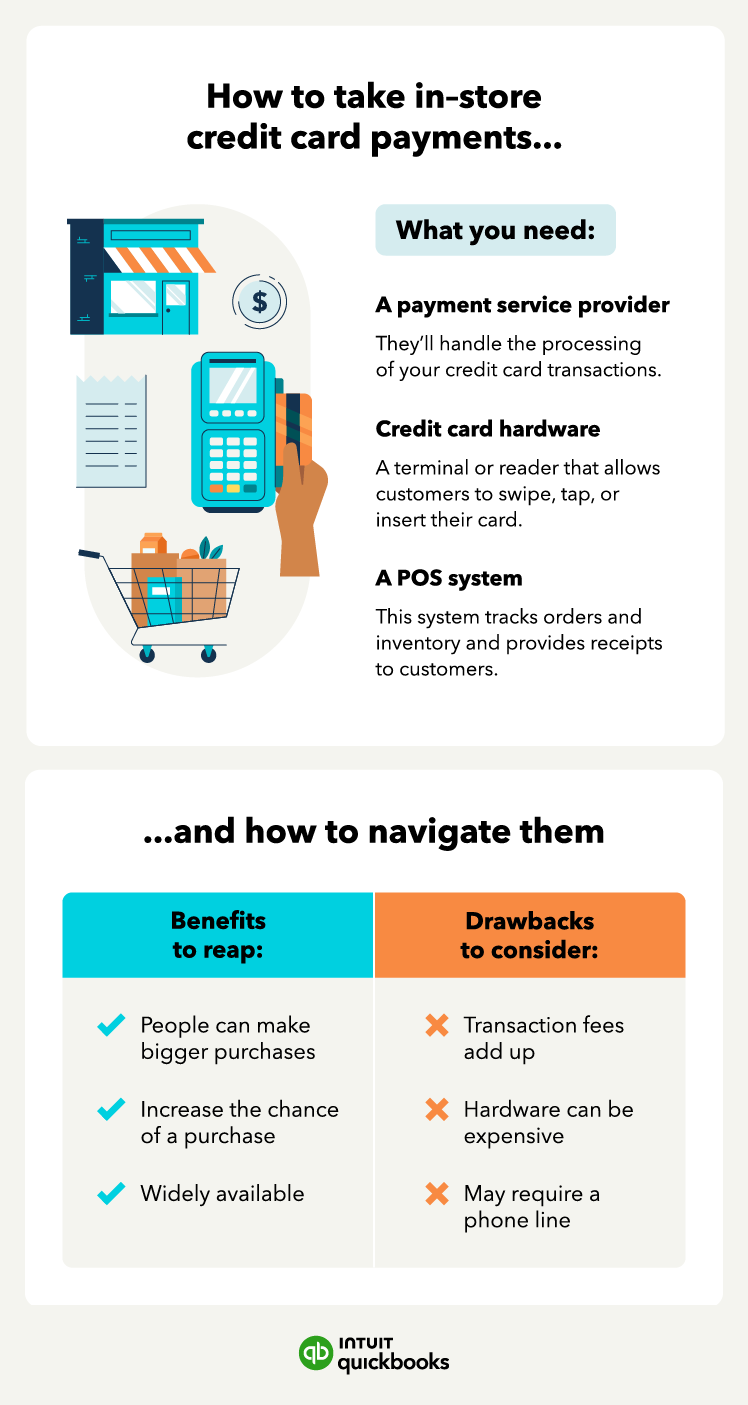

In-store credit card payments

If your business is only a physical location, shop around to see which payment service providers offer the best rates.

If your business is mobile and online, too, you can choose from a wider range of payment processing options, including electronic payments. E-commerce platforms sometimes offer payment processing online and in-person using their hardware (though those options can be limited compared to other systems).

To take credit card payments using credit cards at a brick-and-mortar location, you’ll need one of the following:

- POS system with integrated credit card terminal

- Stand-alone credit card terminal

You should choose your hardware based on the type of business you run. For example, if you operate a convenience store, you’ll probably want terminals that let customers use their cards and enter their PINs. If you own a fine-dining restaurant, you probably need something simpler because your staff will be running customer cards.

Point-of-Sale systems can help you manage sales and inventory and are an important tool for many businesses to have but they aren’t required to take credit cards.

It’s a good idea to take account of the fees you’re responsible for and offer customers other ways to pay. Cash doesn’t have any processing fees. Use a credit card processing fee calculator to determine how much it could cost your business before choosing a provider.

Benefits

- People can make bigger purchases: Accepting credit cards may to larger transactions since customers aren’t limited by their on-hand cash.

- Increase the chance of a purchase: In-person payments still account for 78% of all payments, and many of those are made with credit or debit cards

- Widely available: Credit cards are a dominant payment method, with over 60% of all payments being made by either credit (32%) or debit (30%).

Drawbacks

- Transaction fees add up: Every credit card transaction comes with a fee, and those can add up over time.

- Hardware can be expensive: Buying or renting credit card readers or terminals can be pricey, so it’s an expense you’ll want to factor in.

- May require a phone line: Some systems require a dedicated phone line for processing payments, which could add an extra cost to your operations.

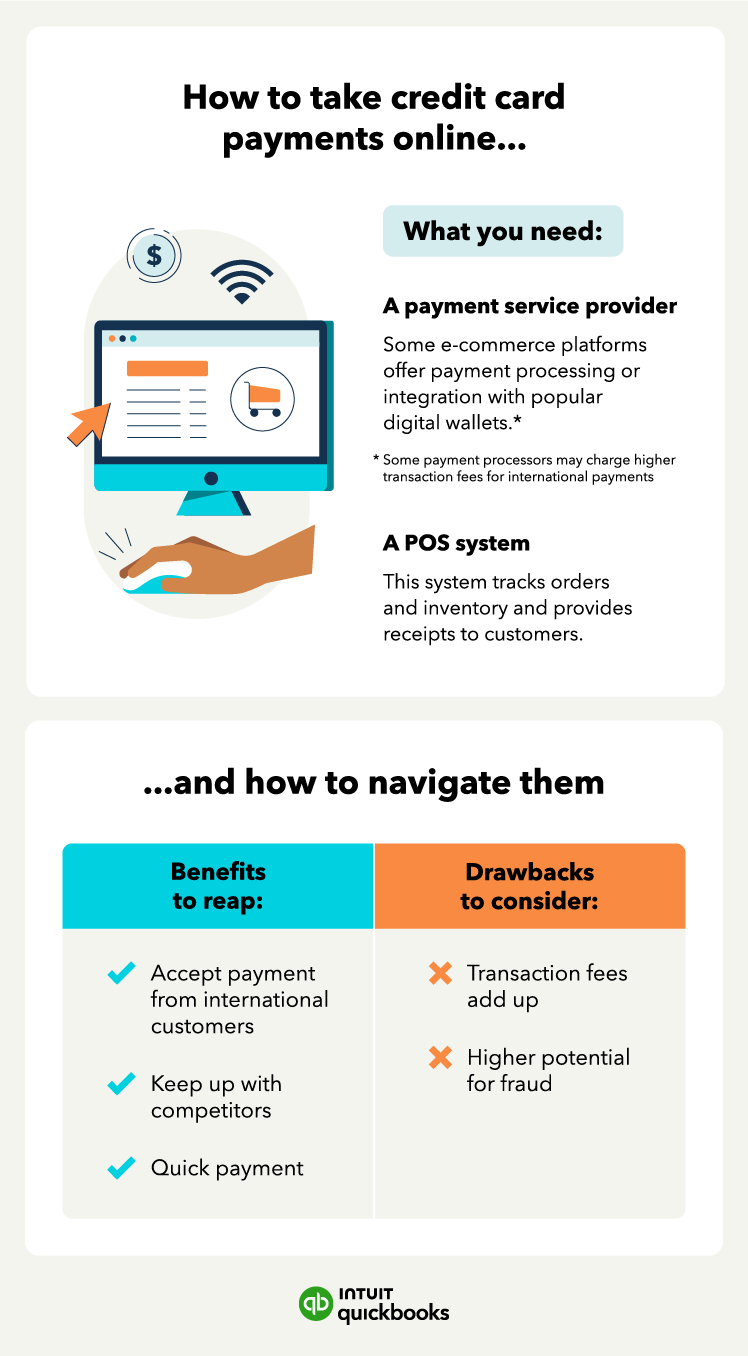

Accept credit card payments online

Your online store might have built-in payment processing or allow you to integrate processing from traditional companies or digital processors. You can also check with other payment service providers.

If your online business has physical locations, you can choose from a wider range of payment processing options. Some e-commerce platforms offer payment processing both online and in-person. You may be limited to using their hardware for in-store or mobile purchases.

Benefits

- Accept payments from international customers: Considering that more than half of online shoppers buy from international sites, you can easily reach customers worldwide and grow your market with online payments.

- Keep up with competitors: According to Forbes, 23% of all retail purchases are expected to happen online by 2027, so offering online payment options is key for staying competitive and meeting customer expectations.

- Quick payments: Online credit card transactions process instantly, which means faster payments and smoother cash flow.

Drawbacks

- Transaction fees add up: Just like in-store payments, online credit card transactions come with processing fees. These fees can build up, especially with high volumes or international payments.

- Higher potential fraud: According to Juniper Research, merchant losses from online payment fraud are expected to exceed $343 billion globally between 2023 and 2027, so make sure you implement strong security measures to protect your business and customers from this growing threat.

Run your business with confidence

Get help and guidance when you need it from real bookkeeping experts at Eric Buchholz Bookkeeping… Get Started right HERE!

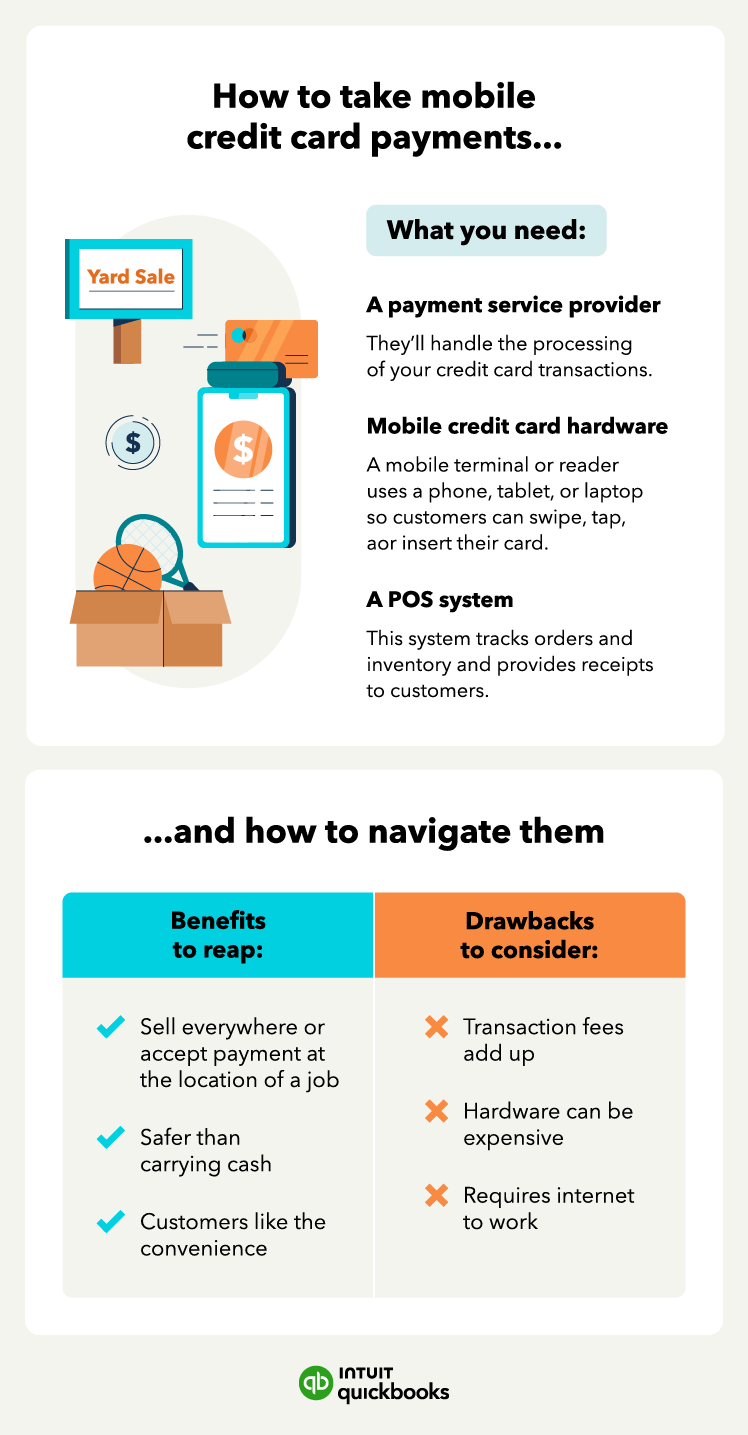

Mobile credit card payments

If your business is strictly mobile commerce, you can choose from several payment processing companies. You can choose a traditional processor with mobile hardware or a digital processor that also provides hardware. If you are mobile and online, check if your online processor offers mobile services.

To accept mobile payments, you’ll need to have a mobile credit card terminal. Because you’ll be dealing with customers in different locations, you may need hardware that lets them enter their PIN.

Benefits

- Sell everywhere or accept payment at the location of a job: You can take payments anywhere your business operates, whether you’re at a customer’s home or on the go.

- Safer than carrying cash: Mobile payments mean you don’t have to carry large amounts of cash, so it’s safer for you and your customers.

- Customers like the convenience: Whether customers tap, swipe, or insert their card, mobile payments make the process quick and easy for them.

Drawbacks

- Transaction fees add up: Just like other credit card payments, mobile transactions come with processing fees that can accumulate over time.

- Hardware can be expensive: Mobile credit card readers and terminals can have upfront or recurring costs, depending on the provider.

- Requires internet to work: You need a reliable internet connection for mobile payment systems to work, which could be a challenge in areas with spotty or no service.

Differences between a merchant account vs. a payment service provider

A merchant account is a bank account that lets your business accept credit card payments. Here’s how it works: when a customer pays with a credit or debit card, the money first goes into your merchant account. During this time, a third-party processor handles the transaction. They typically become available 1-2 days later once the process is complete. After that, the money moves into your business checking account.

On the other hand, a payment service provider (PSP) — e.g., PayPal, Square, Stripe, or QuickBooks Payments — handles all parts of the payment process for you. You don’t need to set up a separate merchant account. Instead, the PSP collects your payments and deposits the funds directly into your bank account. PSPs are easy to use and quick to set up, but they may charge higher fees and offer less flexibility for businesses with larger volumes.

Debit card payments vs credit card payments

While customers don’t see a lot of differences between using credit and debit cards, as a business owner, there are a few things that make them distinct.

Processing networks

Debit card payments are processed through debit card networks like STAR or NYCE, while credit card payments go through credit card networks like Visa or Mastercard.

Fees

Debit card transactions often come with lower fees (0.73% or $0.34 on average, according to the Federal Reserve). On the other hand, credit card transactions tend to have higher fees (1.5% to 3.5%) due to the risks involved and the charges from credit card networks.

Fund availability and authorization process

When customers use a debit card with a PIN, the funds are taken from their account and sent to your merchant account almost immediately. With credit cards or debit cards without a PIN, the funds aren’t transferred until later. It could take a day or two for the money to show up in your account.

Security best practices for accepting credit cards online

Security should be your business’s top priority when accepting online credit payments. Consider these best practices so you can protect your business and customers from data breaches, identity theft, and other fraudulent activities.

PCI compliance

Payment Card Industry Data Security Standard (PCI DSS) is a set of rules for businesses that handle credit card transactions. There are 12 requirements you must follow to ensure your business remains PCI-compliant, which include:

- Install and maintain a firewall configuration to protect cardholder data

- Do not use vendor-supplied defaults for systems passwords and other security parameters

- Protect stored cardholder data

- Encrypt transmission of cardholder data across open, public networks

- Protect all systems against malware and regularly update antivirus software or programs

- Develop and maintain secure systems and applications

- Restrict access to cardholder data by business need to know

- Identify and authenticate access to system components

- Restrict physical access to cardholder data

- Track and monitor access to cardholder data

- Regularly test security systems and processes

- Maintain a policy that addresses information security for all personnel

For more detailed information, the PCI DSS Quick Reference Guide is an excellent resource to review.

Data encryption

Data encryption is another important tool. Encryption turns customer data into unreadable code as it travels through the internet, which makes it harder for hackers to steal. You should use SSL (Secure Socket Layer) or TLS (Transport Layer Security) encryption from the moment a customer enters their payment information until the transaction is complete. For example, Quickbooks Online uses 128-bit SSL encryption to help protect sensitive data from reaching the hands of hackers and other intruders.

Fraud prevention strategies

Fraud prevention should be an ongoing effort for any business that accepts credit cards online. Use tools like Address Verification Systems (AVS), which match the billing address your customer provides with what’s on file at their card issuer. Also, implement the Card Verification Value (CVV) to ensure the person making the payment has the card in hand.

How much do credit card processing fees cost?

Credit card processing fees (also called a merchant discount rate or transaction discount rate) can vary based on your provider but are generally 1.5–3.5%, according to Forbes. This is the fee your business pays to accept credit cards and have your payment processor complete their part of the transaction.

That fee is split up and divided among several parties. These include:

- Interchange: the nonnegotiable fee that the processor and merchant pay to the issuing bank. You’ll usually see this fee as a percentage and a fixed amount (2.5% + $0.25, for example). The percentage goes to the issuing bank, and the network receives the flat fee.

- Assessments: the fees that the credit card networks charge to accept transactions on cards branded with their name. This part of the fee also can’t be negotiated.

- Markups: Markups are a percentage of the overall fee and are charged by your payment processor and bank. These fees help pay for the cost of processing card transactions. It’s possible to negotiate lower markup fees, so check with your PSP and bank.

Another fee you may have to pay on credit card transactions is chargebacks. A chargeback begins if a customer disputes a charge on their card due to fraud or because of an issue with the product or service they received from your company. The issuing bank will then charge you a “retrieval request.” If you are looking for protection from chargebacks, QuickBooks offers Payment Dispute Protection to eligible QuickBooks Payments customers.

If the fee isn’t debited automatically, it’s a good idea to pay these fees quickly because you could get hit with more fees if you don’t respond in the time frame they set in the contract.

You can appeal a chargeback and provide the issuing bank with information to bolster your case. The process can take as long as 4-6 weeks according to Signifyd and it might end with the bank recovering the money originally deposited into your business account. Keeping good records can help the bank rule in your favor.

Choose the best payment setup for your business

There’s a lot that goes into accepting credit cards, but it’s a worthwhile step if you want to boost your sales, improve your customer experience, and manage healthy cash flow.

Fortunately, QuickBooks makes accepting credit card payments straightforward and painless—whether you want to accept them online, by phone, on the go, or even through recurring payments. In addition to credit and debit cards, there are other small business payment methods to consider. Some could save you time and money and help you receive funds faster.

Ready to get started?

Take routine bookkeeping off your never-ending to-do list with the help of a certified professional. At Eric Buchholz Bookkeeping, we can help ensure that your business’s books close every month, and you’re primed for tax season. Our expert certified QuickBooks ProAdvisors have over 25 years of experience working with small business bookkeeping across various industries.

Whether you’re learning security best practices for accepting credit cards online, or weighing your options when it comes to credit card processing fees, Eric Buchholz Bookkeeping can guide you down the right path. Schedule your FREE phone consultation today!… Simply CLICK HERE.