A profit and loss (P&L) statement is the same as an income statement. It’s a financial document that includes a company’s revenues and expenses. Business owners use the P&L to understand how much money a company makes, which they can also quickly and easily do with accounting software.

Knowing how to read a profit and loss statement is key to making informed business decisions. It shows you where you might be able to cut costs. Let’s look at exactly what a P&L is, why it’s important, and how business owners should use it.

What is the format of a profit & loss (P&L) statement?

A profit and loss statement is a snapshot of a company’s sales and expenses over some time, such as one year. It shows company revenues, expenses, and net income over that period. The bottom line on a P&L will be net income, also known as profit or loss.

The profit and loss formula is:

Revenue – Expenses = Profit or loss

There are many ways to format a P&L statement, but all versions include the same basic information. Sales are at the top of the P&L statement, while expenses appear below. The profit or loss is the difference between the two.

Here are the main components of a profit and loss statement:

Revenue

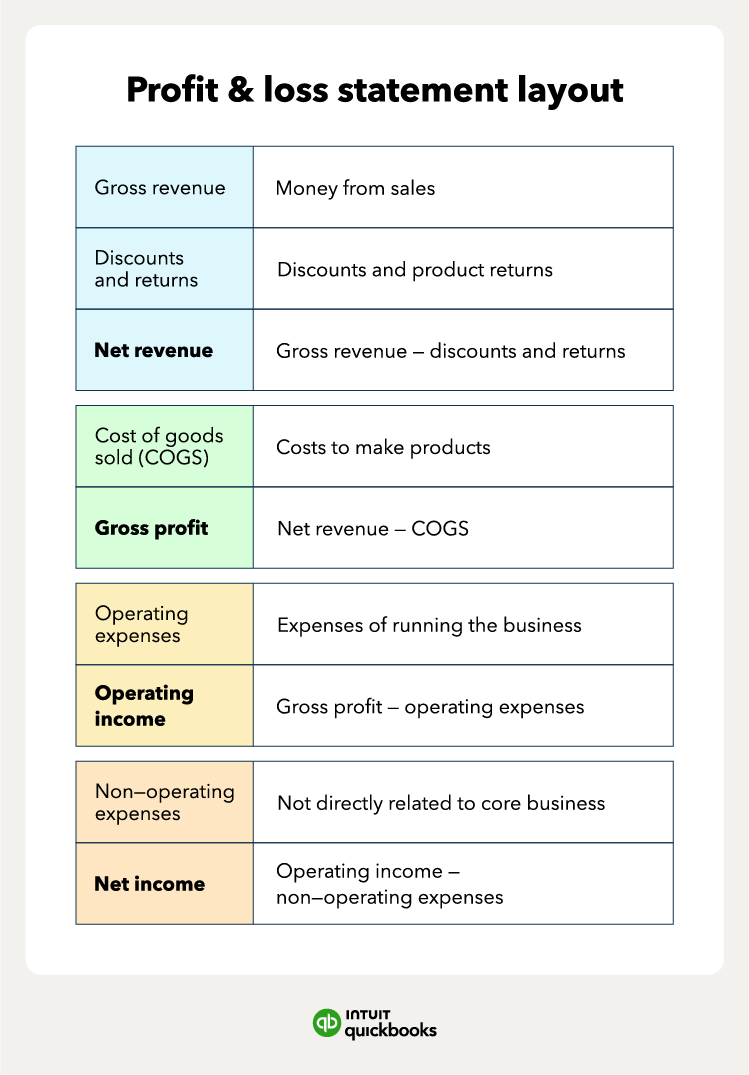

Revenue is the money your business makes from selling goods or services. It’s the very first line on the profit and loss statement. Note there are two types of revenue:

- Gross revenue, or total revenue or sales, is the total amount you make before accounting for discounts, returns, or expenses.

- Net revenue, also known as net sales, is the money you make after deducting discounts and returns.

Note that net revenue is gross revenue minus discounts and returns.

Expenses

The expenses of a business include all the costs to generate revenue.

Cost of goods sold (COGS) is the cost of materials and labor a company uses to make a product or service. It’s also known as the cost of sales. The costs can include raw materials or direct wages for employees. But also certain overhead costs, such as utilities.

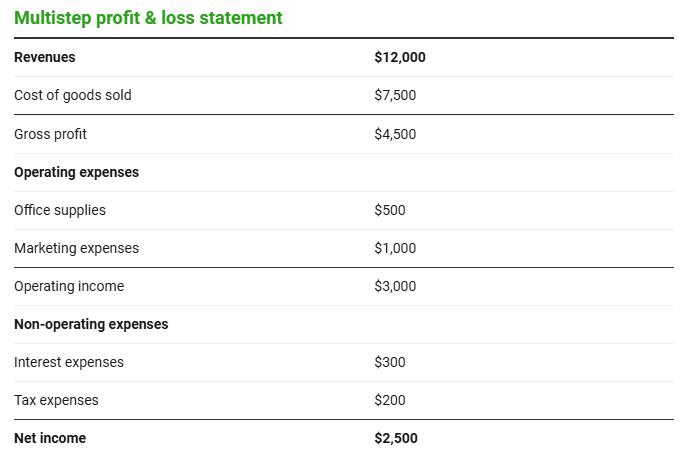

COGS are expenses that show up on the top part of the P&L before gross profit. Gross profit is the money you make from sales after subtracting your cost of goods sold, using the formula:

Gross profit = Net revenue – Cost of goods sold

Other expenses can be operating or non-operating.

Operating expenses are the costs of running your business. While COGS are for making a product, operating expenses are the costs to support that process. Operating expenses include:

- Rent

- Marketing costs

- Salaries for admin staff

- Depreciation

- Licensing fees

Non-operating expenses are costs not part of your core operations. These include taxes, fines, legal fees, and interest. Non-operating expenses include anything unlikely to happen again. For example, losses due to shutting down a business operation.

Income

Income is how much money you make in your business. There are two key types of income—operating and net income.

Operating income is a business’s income from its core operations. It excludes non-operating expenses, such as taxes or interest expenses. This type of income measures how well a company generates money from its main business. The formula for operating income is:

Operating income = Gross profit – Operating expenses

Net income is your bottom line—the last item on your P&L. It’s the money left after subtracting all expenses.

Net income = revenue – COGS – Operating expenses – Non-operating expenses

Net income comes after both operating and non-operating expenses on the P&L. It’s a measure of the money left over for shareholders or owners.

Run your business with confidence

Get help and guidance when you need it from real bookkeeping experts at Eric Buchholz Bookkeeping… Get Started right HERE!

How to put together a profit and loss statement

The P&L will include three key components—revenue, expenses, and income. There are three key steps to making a profit and loss statement.

1. Start with revenue

Determine what period you want to create a profit and loss statement for. This can be any period, but it’s generally best practice to put together a P&L monthly to help identify trends.

You’ll want to calculate your gross revenue for that period and list it on the top line of your P&L.

2. Calculate your costs

After accounting for all your revenues, group your expenses into one of three categories:

- Cost of goods sold (COGS)

- Operating expenses

- Non-operating expenses

COGS are all the costs of making a product. For a service business that doesn’t make a physical product, COGS can include labor for employees performing the service. For example, a hair stylist’s COGS would include the time spent styling hair.

You’ll group all the other costs of running your business as operating expenses. Non-operating expenses should be everything that’s left. This will be the money you spend on things like taxes and interest.

For example, a hairstylist would have operating expenses like cosmetic supplies, insurance, and marketing. Non-operating expenses may include interest on business debt or writing off unsellable inventory.

3. Figure out your net income

This is the last step. It’s subtracting all the expenses from your revenue. The net income will either be a profit or a loss—or, in very rare cases, zero.

How to read a P&L statement

Once you’ve put together your profit and loss statement, it’s useful to analyze it. It’ll show whether you’re profitable or not. But it also allows you to identify areas to save or reduce spending.

Determine profitability

Profitability measures how much a business earns compared to its expenses. There are different ways to measure profitability. Two common measures of profitability are gross profit margin and net profit margin.

Say a window maker’s revenue was $500,000 last year. They spent $300,000 on COGS to make the windows. Net income for the year was $40,000.

The company’s gross profit margin is 40% or ($500,000 – $300,000) / $500,000.

Its net profit margin is 8% or $40,000 / $500,000.

Many small businesses aim for a net profit margin of 10%, although this will depend on your industry.

Assess financial ratios

Beyond profitability, the P&L can also help you calculate other ratios. But you’ll need the help of the balance sheet.

Other key ratios you’ll want to look at are efficiency ratios. These assess how well a company uses its resources. They use one item from the P&L and one from the balance sheet.

The accounts receivable turnover ratio shows how well a business is managing accounts receivable. Accounts receivable is the amount of money that your customers owe you. You’ve already sent them the products but haven’t collected payment yet. Here’s the formula:

Accounts receivable turnover = Sales / Average accounts receivable

A low or declining accounts receivable turnover shows a declining ability to collect customer payments.

The inventory turnover ratio tells how well a company is managing inventory, and the formula is:

Inventory turnover ratio = Cost of goods sold / Average inventory

You can also use an inventory turnover calculator to help you see how your business is doing.

Comparing P&L statements

P&L statements are most useful when comparing them to previous periods because they allow you to track progress over time. They’re also useful when it comes to setting goals for your business.

You can also compare your P&L to companies in your industry. This will help you determine where you stand relative to other businesses.

You can also compare your P&L to companies in your industry. This will help you determine where you stand relative to other businesses.

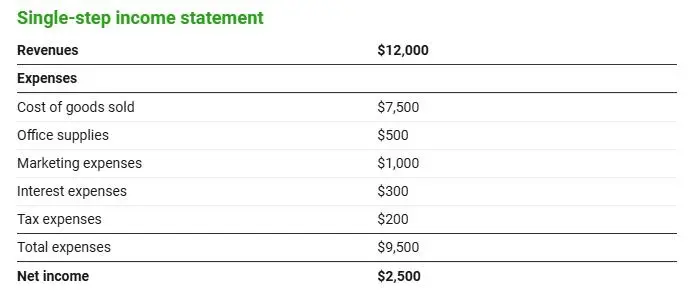

Example of a profit and loss statement

The single-step method of putting together a P&L statement is simple, straightforward, and involves only one calculation. This method subtracts all expenses from revenues to get net income—it doesn’t separate revenues and expenses into different categories.